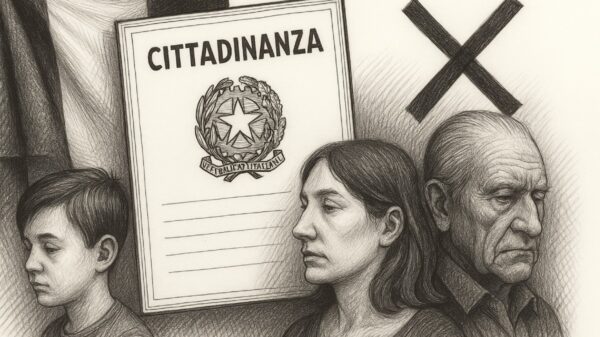

A Italian Supreme Court of Cassation decided that non-resident foreigners in the country do not need a 'Fiscal Code' to request free sponsorship or to pay legal costs.

This decision is a relief for applicants in the process of recognition of Italian citizenship, who faced the demands of 'Fiscal Code' — equivalent to the Brazilian CPF — in some Italian courts.

Many descendants recognized as Italian citizens found it difficult to exercise their rights due to the slowness of bureaucratic procedures after the sentence.

The case in point

The Court of Roma rejected the request for free justice made by a Romanian citizen, basing its decision on the absence of the Italian tax code in the request.

According to the court, the lack of this document made the request inadmissible under art. 79 of DPR 155/2002. The applicant had informed his Romanian tax code and his address abroad, but the Court understood that, to be admitted, the request must contain the Italian tax code, obtained from the Inland Revenue.

Unsatisfied with the decision, the Romanian appealed to the Supreme Court of Cassation, claiming that the requirement of the Italian tax code violated the law.

The appellant based his appeal on the interpretation of the Constitutional Court, which, in sentence no. 144/2004, had already established the possibility for non-resident foreigners to request free justice, simply by indicating their domicile abroad.

Analysis and decision of the Court of Cassation

A Court of Cassation, in a decision of 23/07/2024 (sentence 30047), accepted the appeal, highlighting that art. 6, paragraph 2, of DPR 605/1973, already provides that the obligation to indicate the tax code for non-residents can be fulfilled only by indicating basic personal data, in accordance with art. 4, except tax domicile.

This data includes name, surname, place and date of birth, gender and, instead of tax domicile, domicile or legal headquarters abroad. The appellant, who was on a short stay in Italy (only 40 days), did not have an Italian tax identification number, but only that of his country of origin.

The Court of Cassation concluded that, for non-resident foreigners, including those from countries of European Union, it is sufficient to provide basic personal data and domicile abroad.

There is no obligation for these foreigners to obtain an Italian tax code to request free sponsorship, as long as they present income data in accordance with the last declaration in the country of residence, in accordance with art. 70 of DPR 115/2002.

Implications of the decision

The decision of the Supreme Court of Cassation, of July 23, 2024, annuls the need for the Italian tax code, expanding access to free sponsorship for non-resident foreigners and eliminating a bureaucratic obstacle that many faced at the end of the recognition process of the Italian citizenship, when they needed to pay taxes to make the sentence final.

FOLLOW-US